As per Rule 46 of the CGST Rules, 2017, every registered person supplying taxable goods or services or both must issue a tax invoice as prescribed under Section 31 of the CGST Act, 2017. The rule prescribes mandatory contents of the tax invoice, including various exceptions, export invoice guidelines, e-invoice provisions, and QR code requirements.

Rule 46 of the Central Goods and Services Tax (CGST) Rules, 2017, combined with Section 31 of the CGST Act, prescribes the essential protocol that every GST-registered business in India must follow to issue a valid tax invoice. These provisions ensure transparency, compliance, and seamless Input Tax Credit (ITC) flow under GST.

Why is the GST Tax Invoice So Crucial?

A GST tax invoice is much more than a routine document—it’s statutory proof of supply and the gateway to ITC for buyers. Issuing an incomplete or non-compliant invoice can lead to:

- Rejection of ITC claims

- Penalties for the supplier

- Disputes or delays in GST audits

When Should a GST Tax Invoice Be Issued? (As per Section 31)

- For Goods:

- With movement: Before or at the time of removal

- No movement: At the time goods are made available to recipient

- For Services:

- Within 30 days (45 days for banks, financial institutions)

- Value below ₹200: Not mandatory unless invoice is demanded

Latest GST Invoice Compliance Essentials

- Always check for the latest CBIC/HSC updates on HSN/SAC digit reporting.

- Revised invoices can be issued within a month of GST registration if needed.

- For exports, invoice must be properly endorsed and include required declarations.

- For mixed supply (exempt + taxable), an invoice-cum-bill of supply is allowed.

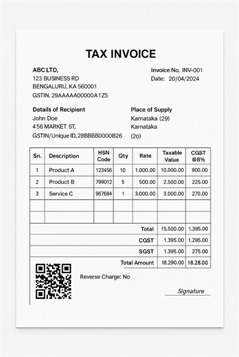

Mandatory Fields in a GST Tax Invoice (Rule 46 Highlights)

To ensure your invoice is compliant and maximizes ITC eligibility, always include these essentials:

| Field Name | Description |

| Supplier Details | Name, address, and unique GSTIN of supplier |

| Invoice Number & Date | A unique serial number (not more than 16 characters) and clear date of issue |

| Recipient Information | Name, address, and GSTIN (if registered); for B2C > ₹50,000, add place of supply with state and code |

| HSN/SAC Code | HSN for goods or SAC for services as per the notified requirement |

| Item Description | Specific details of goods/services |

| Quantity & Unit | Include for goods; use relevant measuring unit |

| Total Value & Taxable Value | Gross and taxable values, after discounts |

| GST Rates & Tax Amounts | Tax breakdown—CGST, SGST/UTGST, IGST, cess—displayed clearly |

| Place of Supply & Delivery Address | Mandatory for inter-State or bill-to-ship-to transactions |

| Reverse Charge Indicator | Mention if transaction is under reverse charge |

| Signature/Digital Signature | Mandatory unless it’s an e-invoice under GSTN |

| Invoice Endorsement for Export/SEZ | Mark “Supply meant for export/sez…” if outward supply is to SEZ or overseas customer |

Pro Tip: Digital or e-invoices also require an Invoice Reference Number (IRN) & QR code as notified.

Export or SEZ Invoices – Additional Provisions:

As per amended provisions:

The invoice must carry the endorsement:

- “SUPPLY MEANT FOR EXPORT/SUPPLY TO SEZ UNIT OR SEZ DEVELOPER FOR AUTHORISED OPERATIONS ON PAYMENT OF INTEGRATED TAX”

OR

- “SUPPLY MEANT FOR EXPORT/SUPPLY TO SEZ UNIT OR SEZ DEVELOPER FOR AUTHORISED OPERATIONS UNDER BOND OR LETTER OF UNDERTAKING WITHOUT PAYMENT OF INTEGRATED TAX”

🔁 Instead of clause (e), the following is mandatory for export invoices:

- (i) Name and address of the recipient

- (ii) Address of delivery

- (iii) Name of the country of destination

[Ref: Notification No. 17/2017-CT dated 27.07.2017]

E-Invoice and Digital Signature Relaxation:

- Where e-invoice is issued as per Information Technology Act, 2000, signature/digital signature is not mandatory.

[Inserted via Notification No. 74/2018-CT dated 31.12.2018]

QR Code Requirement (For B2C e-invoice):

Government may mandate QR code on invoice through a notification, subject to specific conditions/restrictions.

[Ref: Notification No. 31/2019-CT dated 28.06.2019]

Consolidated Tax Invoice (B2C)

✅ When allowed:

As per proviso to Rule 46, a registered person may not issue an individual tax invoice in the following cases:

- Recipient is not registered, and

- Recipient does not require such invoice

➡️ In such case, the supplier shall issue a Consolidated Tax Invoice at end of each day covering such supplies.

⛔Exception:

This relaxation is not available to suppliers making supply of cinema tickets in multiplexes.

📑Inserted by:

Notification No. 33/2019-CT dated 18.07.2019

(effective from 01.09.2019)